Living debt-free is a dream many people have. Some consumer financial gurus have built their fortunes on selling “systems” to consumers that help them to get out of debt. But getting out of debt and staying out of debt are two different things. Your lifestyle may change over time, and your financial needs may change, too.

Living debt-free is a dream many people have. Some consumer financial gurus have built their fortunes on selling “systems” to consumers that help them to get out of debt. But getting out of debt and staying out of debt are two different things. Your lifestyle may change over time, and your financial needs may change, too.

Just because you pay off all your debts doesn’t mean you’ll never have to go into debt again. In fact, many people who pay off all their debts may incur new debts within 1-2 years, and if they are fiscally responsible consumers they will pay off those debts very quickly, too.

Going into debt is not necessarily a bad thing if it means you can buy a good house or a good vehicle. But what many people don’t realize is that in order to qualify for the best interest rates you need to demonstrate to lenders that:

- You can pay your debts responsibly

- You can manage your debt-to-income ratio

- You are committed to participating in the consumer credit economy

Closing all your credit cards once you pay them off (in your quest to live debt-free) is thus a mistake, unless you are very certain you will be able to save up enough money to buy all the things you need.

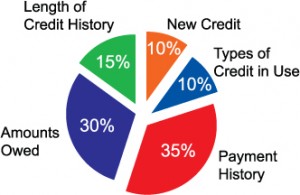

One of the most important factors that potential lenders look at when you apply for credit is how much available credit you currently have. The more available (unused) credit you have, the easier it is for you to qualify for the best interest rates and repayment terms. People who close their credit card accounts deprive themselves of the best opportunities.

For most people, then, the goal should not be to live debt-free but rather to live with debt that matches the best available terms on the market. To do this you need to:

- Spend less than you make

- Save or invest what you don’t spend

- Keep your credit balances as low as possible

- Aggressively pay down your debts whenever possible

- Live by a budget that ensures you don’t miss payments even during financial distress

It’s not easy to do all that. If you sell consumers your financial wisdom and make millions of dollars in the process you’ll find it easier to live debt-free, but most people have to keep the debt monster at bay by carefully managing their monthly income.

Before you take the irrevocable step of closing a credit account, ask yourself how much credit you think you’ll need to apply for in the next five years. Once you close those accounts your credit scores will be adjusted downward to reflect your new available credit. It can take 1-2 years to rebuild a credit score to the point where you qualify for the best available interest rates on mortgages.

What we do not want to do is live with a constant burden of debt. That is, it’s not necessary to maintain a balance on your credit cards in order to keep them active. Once you have fully paid off your credit cards it is better to only use them sparingly and to pay off the balances as quickly as possible. This way you pay as little interest as possible on the money you borrow.

If you can save enough money to live without credit, then more power to you. Most consumers simply will not be able to do that. So the majority of people will do better to learn how to manage their credit. Managing credit is the not the same thing as managing debt. Credit represents how much you can potentially borrow. Debt represents how much you have borrowed.